1QFY2017 Result Update | HFC

July 26, 2016

Dewan Housing Finance Corporation

BUY

CMP

`225

Performance Highlights

Target Price

`270

Particulars (` cr)

1QFY17 4QFY16

% chg (qoq) 1QFY16

% chg (yoy)

Investment Period

12 months

NII

483

486

(0.6)

418

15.5

Pre-prov. profit

348

333

4.5

293

18.6

Stock Info

PAT

201

190

6.2

173

16.2

Source: Company, Angel Research

Sector

HFC

For 1QFY2017, Dewan Housing Finance Corporation (DHFL) reported a 16%

Market Cap (` cr)

6,568

growth in PAT to `201cr, which is in line with our expectation. There has been a

Beta

1.6

decline in the company’s cost structure after many quarters, which we believe is

sustainable and would add to earnings growth going ahead. At the operating

52 Week High / Low

268/140

level, the performance remained decent.

Avg. Daily Volume

2,002,386

Loan growth remains decent: The company’s AUM as of 1QFY2017 end was up

Face Value (`)

10

20% on a yoy basis at `72,012cr. While sanctions grew by a moderate 12% yoy,

disbursements at `6,215cr witnessed a strong 26% yoy growth during the quarter.

BSE Sensex

28,095

The company securitized loans worth `1,152cr during the quarter and the

Nifty

8,635

portfolio of securitized loans accounted for 12% of the total AUM.

Reuters Code

DWNH.BO

Project loans growing faster than the overall loan portfolio: Loans to individuals

which account for ~71.5% of the AUM, grew by 15.2% yoy during the quarter.

Bloomberg Code

DEWH.IN

The company continued to aggressively expand its non-individual loan book,

which is evident from the 93% yoy growth in loans to projects. The segment

accounted for 9.8% of the AUM compared to 9% at the end of 4QFY2016 and vs

Shareholding Pattern (%)

6.1% in 1QFY2016. We believe the company will continue to expand the high

yielding developer loan book in the near term.

Promoters

34.9

Asset quality marginally weakened but still comfortable: DHFL has been able to

MF / Banks / Indian Fls

2.6

maintain a stable asset quality over the last few quarters. During the quarter

FII / NRIs / OCBs

32.2

under review, GNPAs rose to 0.98% vs 0.93% as at the end of 4QFY2016. On a

yoy basis, provisions were up 41%, which we feel is reasonable, looking at the

Indian Public / Others

30.3

strong growth in non-individual loan book which is subject to stricter regulatory norms

in terms of provisioning. NPAs from the individual loans segment stood at 0.74%

while that from the non-individual segment stood at 1.24% (LAP, Project Loans, and

Abs. (%)

3m

1yr

3yr

SME combined). We don’t expect any deterioration in asset quality in the near term.

Sensex

7.6

(2.5)

38.0

Margins as well as return ratios likely to remain stable: Though the cost of funds

has declined, the yield too has come down in the last quarter due to competitive

DHFL

9.8

(4.7)

192.2

intensity. This resulted in the NIM declining to 2.91% compared to 2.96% in

4QFY2016. We believe increasing exposure to the high yielding project loans and

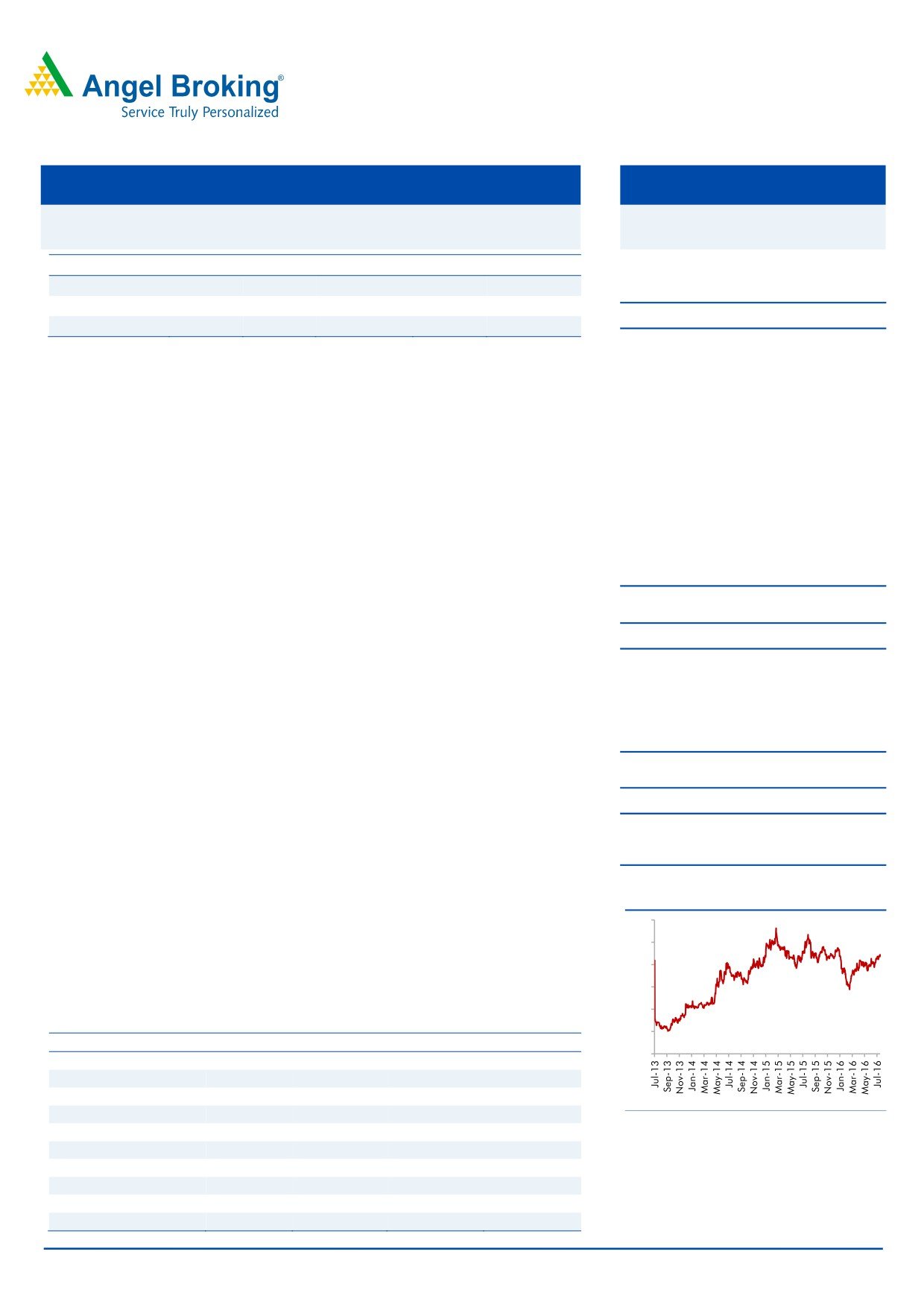

3-Year Daily Price Chart

LAP portfolio will enable the company to maintain its NIM above 2.9% levels.

300

Outlook and valuation: We expect the company to post a healthy loan book

250

CAGR of 20% over FY2015-18E which is likely to translate in an earnings CAGR

of 21.3% over the same period. Despite a 19% run up in the stock price since we

200

initiated coverage, the stock is still attractively valued at a little above 1x FY2018E

150

ABV. We maintain our BUY on the stock and retain our target price of `270.

100

Key financials (standalone)

50

Y/E March (` cr)

FY2015

FY2016

FY2017E

FY2018E

0

NII

1,256

1,664

2,050

2,500

% chg

41.5

32.5

23.2

21.9

Net profit

620

729

866

1,084

% chg

17.8

17.7

18.5

25.3

Source: Company, Angel Research

NIM (%)

2.8

2.9

2.9

2.9

EPS (`)

21.3

24.9

29.7

34.6

P/E (x)

10.6

9.0

7.6

6.5

P/ABV (x)

1.6

1.4

1.2

1.0

Siddharth Purohit

RoA (%)

1.3

1.2

1.1

1.2

022 - 3935 7800 Ext: 6872

RoE (%)

15.1

14.7

15.4

16.2

Source: Company, Angel Research; Note: CMP as of July 25, 2016

Please refer to important disclosures at the end of this report

1

Dewan Housing Finance | 1QFY2017 Result Update

Exhibit 1: 1QFY2017 performance (standalone)

Particulars (` cr)

1QFY17

4QFY16

% chg (qoq)

1QFY16

% chg (yoy)

FY2016

FY2015

% chg

Interest earned

1,958

1,964

(0.3)

1,652

19.0

7,312

5,979

22.0

Interest expenses

1,475

1,479

(0.2)

1,234

19.5

5,490

4,460

23.1

Net interest income

483

486

(0.6)

418

15.5

1,822

1,519

19.9

Non-interest income

1

2

(50.0)

1

10.6

5

3

82.4

Operating income

484

488

(0.8)

419

15.5

1,827

1,522

20.0

Operating expenses

136

155

(12.2)

126

8.4

550

474

15.9

Pre-prov. profit

348

333

4.5

293

18.6

1,277

1,048

21.9

Provisions & cont.

45

50

(10.0)

32

40.6

175

105

66.7

PBT

303

283

7.0

261

15.9

1,102

943

16.9

Prov. for taxes

102

93

8.7

88

15.2

373

322

15.9

PAT

201

190

6.2

173

16.2

729

621

17.4

EPS (`)

6.9

6.5

6.2

5.9

16.1

24.9

21.3

16.9

Cost-to-income ratio (%)

28.1

31.8

30.0

30.1

31.1

Effective tax rate (%)

33.5

33.0

33.7

33.8

34.1

Source: Company, Angel Research

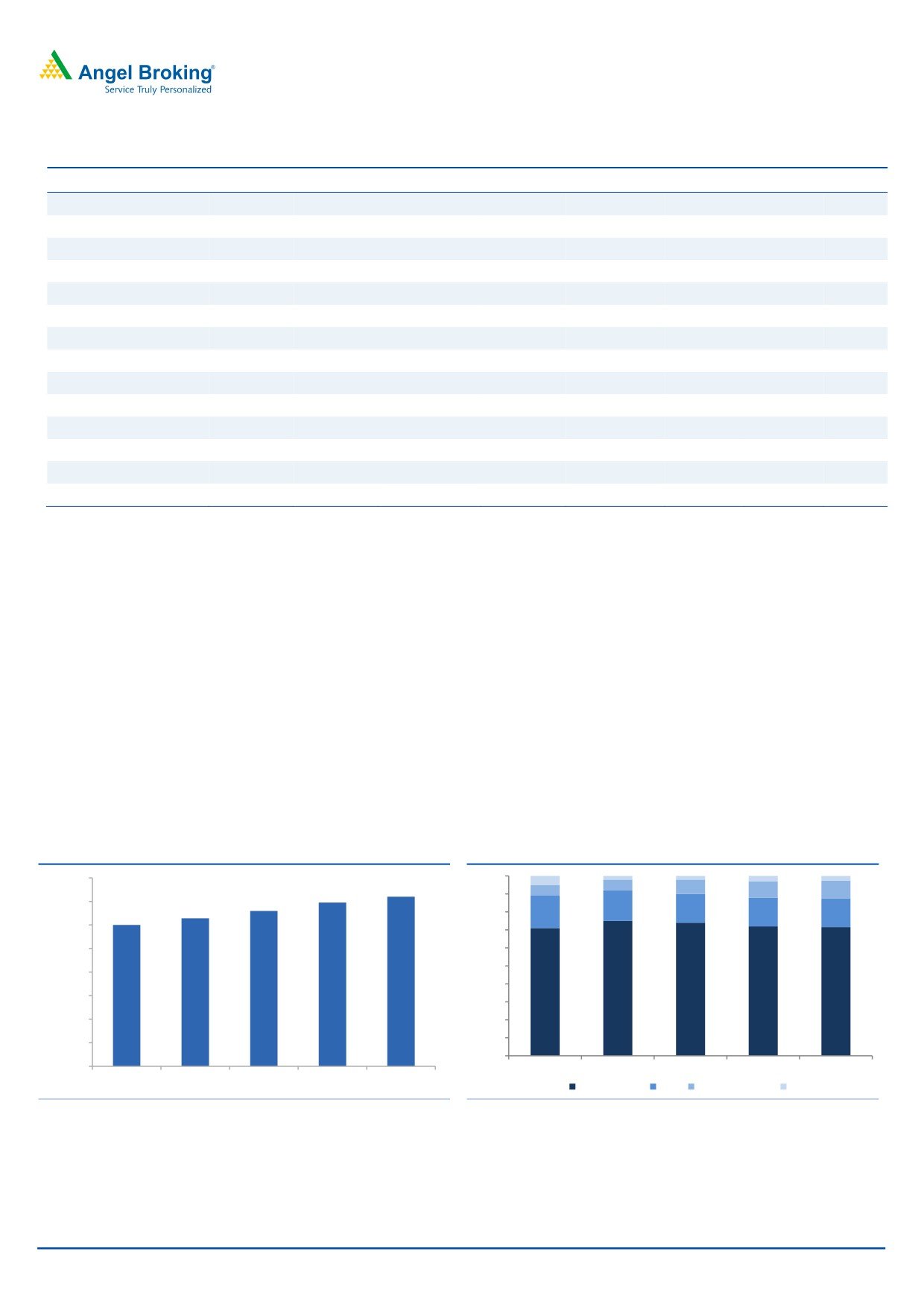

Loan growth remained decent: The company’s AUM as of 1QFY2017 end was up

20% on a yoy basis at `72,012cr. While sanctions grew by a moderate 12% yoy,

disbursements at `6,215cr witnessed a strong 26% yoy growth during the quarter.

The company securitized loans worth `1,152cr during the quarter and the portfolio

of securitized loans accounted for 12% of the total AUM.

Project loans continued to grow faster than overall loan: Loans to individuals which

account for ~71.5% of the AUM, grew by 15.2% yoy during the quarter. The

company continued to aggressively expand its non-individual loan book, which is

evident from the 93% yoy growth in loans to projects. The segment accounted for

9.8% of the AUM compared to 9% as at the end of 4QFY2016 and vs 6.1% in

1QFY2016. We believe the company will continue to expand the high yielding

developer loan book in the near term.

Exhibit 2: AUM growth remains strong

Exhibit 3: Loan Mix

80,000

100%

72,012

6%

8%

69,524

6%

9%

10%

65,962

90%

70,000

62,837

17%

16%

60,002

80%

18%

16%

16%

60,000

70%

50,000

60%

50%

40,000

40%

71%

75%

74%

72%

72%

30,000

30%

20,000

20%

10%

10,000

0%

-

1QFY16

2QFY16

3QFY16

4QFY16

1QFY17

1QFY16

2QFY16

3QFY16

4QFY16

1QFY17

Home Loans LAP Project Finance

Others

Source: Company, Angel Research

Source: Company, Angel Research

July 26, 2016

2

Dewan Housing Finance | 1QFY2017 Result Update

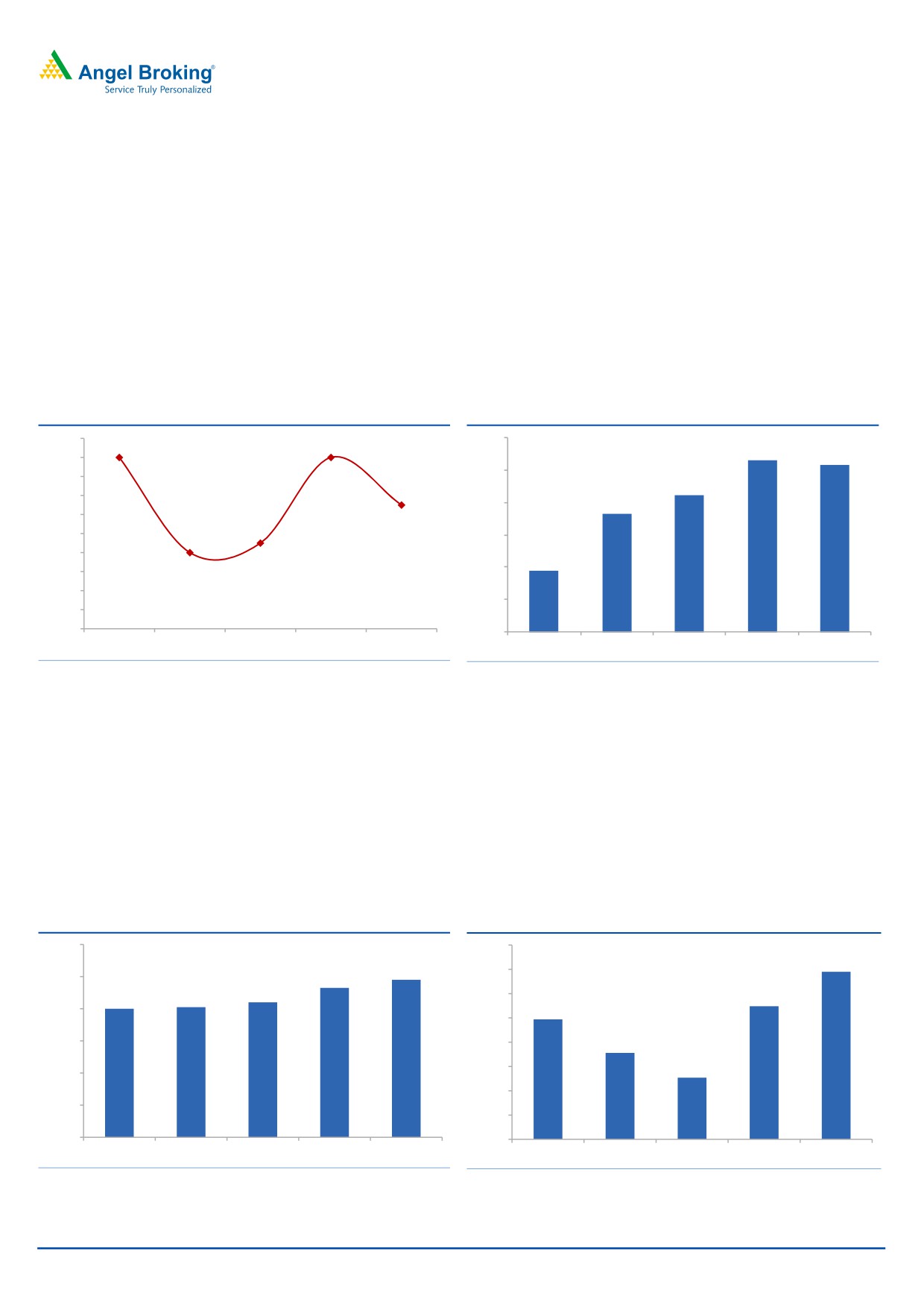

Margins as well as return ratios likely to remain stable: Though the cost of funds

has declined, the yield too has come down in the last quarter due to competitive

intensity. This resulted in the NIM declining to 2.91% compared to 2.96% in

4QFY2016. We believe increasing exposure to the high yielding project loans and

LAP portfolio will enable the company to maintain its NIM above 2.9% levels. We

estimate the company to deliver a ROA of 1.2% and ROE of 16% by FY2018.

The company received a refund of `250cr from a developer after a change in the

latter’s construction plans who now expects to complete the construction in

2-3 years. The release of funds and completion of the building would be a positive

development for the company.

Exhibit 4: Marginal decline in NIM

Exhibit 5: NII growth trend remains healthy

500

2.98%

486

483

2.96%

2.96%

2.96%

480

2.94%

465

2.92%

2.91%

460

453

2.90%

2.88%

440

2.87%

2.86%

2.86%

418

420

2.84%

2.82%

400

2.80%

2.78%

380

1QFY16

2QFY16

3QFY16

4QFY16

1QFY17

1QFY16

2QFY16

3QFY16

4QFY16

1QFY17

Source: Company, Angel Research

Source: Company, Angel Research

Asset quality marginally weakened but still comfortable: DHFL has been able to

maintain a stable asset quality over the last few quarters. During the quarter under

review, GNPAs rose to 0.98% vs 0.93% as at the end of 4QFY2016. On a yoy

basis, provisions were up 41%, which we feel is reasonable, looking at the strong

growth in non-individual loan book which is subject to stricter regulatory norms in

terms of provisioning. NPAs from the individual loans segment stood at 0.74%

while that from the non-individual segment stood at 1.24% (LAP, Project Loans,

and SME combined). We don’t expect any deterioration in asset quality in the near

term.

Exhibit 6: Asset quality weakened marginally

Exhibit 7: Adequately Capitalised

1.20%

18.0%

17.5%

0.98%

17.5%

1.00%

0.93%

0.84%

0.80%

0.81%

17.0%

16.7%

0.80%

16.5%

16.5%

0.60%

16.0%

15.8%

15.3%

15.5%

0.40%

15.0%

0.20%

14.5%

0.00%

14.0%

1QFY16

2QFY16

3QFY16

4QFY16

1QFY17

1QFY16

2QFY16

3QFY16

4QFY16

1QFY17

Source: Company, Angel Research

Source: Company, Angel Research

July 26, 2016

3

Dewan Housing Finance | 1QFY2017 Result Update

Outlook and valuation

We expect the company to post a healthy loan book CAGR of 20% over

FY2015-18E which is likely to translate into an earnings CAGR of 21.3% over the

same period. Despite a 19% run up in the stock price since we initiated coverage,

the stock is still attractively valued at a little above 1x FY2018E ABV. We maintain

our BUY on the stock and retain our target price of `270.

Company Background

DHFL was established in 1984 by late Shri Rajesh Kumar Wadhawan. The

company is a dominant player in niche markets (tier II & III cities) with strong

foothold in the limited competition low and middle income (LMI) segment. After the

acquisition and merger of First Blue Home Finance, DHFL also now caters to the

middle and upper middle income group. The company operates in the mortgage

financing business where the growth and asset quality have remained healthy over

the past few years.

The company has emerged as a one-stop-shop for its customers’ financial needs,

extending beyond home loans. It has a presence in education loans, life insurance,

and mutual funds segments through Avanse Education Loans, DHFL Pramerica Life

Insurance and DHFL Pramerica Asset Managers Pvt Ltd, respectively.

It is India’s third largest private sector housing finance company with an AUM of ~

`72,000cr (as on June 30, 2016). The company has a well diversified loan book

with housing loans accounting for the largest share at 72%, followed by LAP (16%),

project loans (9.8%) and loans to SME (2.6%) (as of June 30, 2016).

The company currently has a strong distribution network with pan-India presence

and 2 international representative offices in the UK and the UAE. It operates via a

large distribution network of 362 company operated centers across India and 357

locations through alliance partners with the distribution network focused primarily

on tier II and tier III locations.

July 26, 2016

4

Dewan Housing Finance | 1QFY2017 Result Update

Income statement (standalone)

Y/E March (` cr)

FY2013 FY2014 FY2015

FY2016

FY2017E

FY2018E

NII

678

888

1,256

1,664

2,050

2,500

- YoY Growth (%)

70.0

30.9

41.5

32.5

23.2

21.9

Other Income

280

296

265

164

175

188

- YoY Growth (%)

11.7

5.8

(10.5)

(38.3)

7.1

7.4

Operating Income

958

1,184

1,522

1,828

2,225

2,688

- YoY Growth (%)

47.5

23.6

28.5

20.1

21.7

20.8

Operating Expenses

304

384

480

550

637

731

- YoY Growth (%)

22.3

26.2

25.2

14.5

15.8

14.7

Pre - Provision Profit

654

801

1,041

1,278

1,588

1,957

- YoY Growth (%)

63.1

22.4

30.1

22.7

24.3

23.2

Prov. & Cont.

45

66

99

175

274

311

- YoY Growth (%)

89.9

47.7

48.7

77.4

56.2

13.5

Profit Before Tax

609

734

943

1,102

1,314

1,646

- YoY Growth (%)

61.4

20.5

28.4

16.9

19.2

25.3

Prov. for Taxation

159

206

322

373

449

562

- as a % of PBT

26.1

28.1

34.1

33.8

34.1

34.1

PAT

459

527

620

729

866

1,084

- YoY Growth (%)

60.9

14.8

17.8

17.6

18.7

25.3

Balance sheet (standalone)

Y/E March (` cr)

FY2013 FY2014 FY2015

FY2016

FY2017E

FY2018E

Share Capital

128

128

146

292

292

313

Reserve & Surplus

3,109

3,447

4,490

4,725

5,456

6,850

Loan Funds

27,441

33,890

40,526

49,800

61,730

76,519

- Growth (%)

61.9

23.5

19.6

22.9

24.0

24.0

Other Liab. & Prov.

5,172

6,465

9,557

13,115

15,400

18,246

Total Liabilities

35,850

43,930

54,718

67,933

82,878

1,01,928

Investments

275

721

1,006

1,249

1,524

4,080

Advances

32,403

38,651

48,789

60,572

73,898

88,677

- Growth (%)

77.5

19.3

26.2

24.2

22.0

20.0

Fixed Assets

438

988

985

1,222

1,491

1,834

Other Assets

2,735

3,569

3,938

4,889

5,965

7,336

Total Assets

35,850

43,930

54,718

67,933

82,878

1,01,928

July 26, 2016

5

Dewan Housing Finance | 1QFY2017 Result Update

Ratio analysis (standalone)

Y/E March

FY2013

FY2014

FY2015

FY2016

FY2017E

FY2018E

Profitability ratios (%)

NIMs

2.6

2.4

2.8

2.9

2.9

2.9

Cost to Income Ratio

31.7

32.4

31.6

30.1

28.6

27.2

RoA

1.6

1.3

1.3

1.2

1.1

1.2

RoE

17.4

15.5

15.1

15.1

16.1

16.8

Asset Quality (%)

Gross NPAs

0.73

0.8

1.0

1.1

1.2

1.3

Net NPAs

0.48

0.5

0.7

0.8

0.8

0.8

Provision Coverage

34.2

33.5

28.7

31.5

33.1

38.6

Per Share Data (`)

EPS

17.9

20.5

21.3

24.9

29.7

34.6

ABVPS (75% cover.)

118.7

129.0

143.7

162.0

184.0

215.3

DPS

1.0

1.6

1.1

0.6

0.8

0.9

Valuation Ratios

PER (x)

12.6

11.0

10.6

9.0

7.6

6.5

P/ABVPS (x)

1.9

1.7

1.6

1.4

1.2

1.0

Dividend Yield

0.4

0.7

0.5

0.3

0.4

0.4

DuPont Analysis

NII

2.4

2.2

2.5

2.7

2.7

2.7

(-) Prov. Exp.

0.2

0.2

0.2

0.3

0.4

0.3

Adj. NII

2.2

2.1

2.3

2.4

2.4

2.4

Treasury

0.0

0.0

0.0

0.0

0.0

0.0

Int. Sens. Inc.

2.2

2.1

2.4

2.4

2.4

2.4

Other Inc.

0.9

0.7

0.5

0.3

0.2

0.2

Op. Inc.

3.2

2.8

2.9

2.7

2.6

2.6

Opex

1.1

1.0

1.0

0.9

0.8

0.8

PBT

2.1

1.8

1.9

1.8

1.7

1.8

Taxes

0.6

0.5

0.7

0.6

0.6

0.6

RoA

1.6

1.3

1.3

1.2

1.1

1.2

Leverage

10.9

11.7

12.0

12.7

14.0

14.3

RoE

17.1

15.5

15.1

15.1

16.1

16.8

July 26, 2016

6

Dewan Housing Finance | 1QFY2017 Result Update

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange Limited. It is also registered as a Depository Participant with CDSL

and Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is a

registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates/analyst has not received any compensation / managed or co-managed public

offering of securities of the company covered by Analyst during the past twelve months.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals. Investors are advised to refer the Fundamental and Technical Research Reports available on our website to evaluate the

contrary view, if any.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Disclosure of Interest Statement

Dewan Housing Finance

1. Financial interest of research analyst or Angel or his Associate or his relative

No

2. Ownership of 1% or more of the stock by research analyst or Angel or associates or relatives

No

3. Served as an officer, director or employee of the company covered under Research

No

4. Broking relationship with company covered under Research

No

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15)

July 26, 2016

7